This view is reinforced by Ind AS 16, Property, plant and equipment, which also mandates component accounting. This therefore implies that, companies would have to break up their tangible assets into various components (physical component or a non-physical component that represents a major inspection or overhaul) for computation of depreciation. This will require considerable efforts since management would have to estimate value of components as on 1st April 2015. For compliance with schedule II, components will need to be identified for the opening block of assets as at 1st April 2015 and cannot be restricted only to new assets acquired on or after adoption of component approach.

Identification of Components

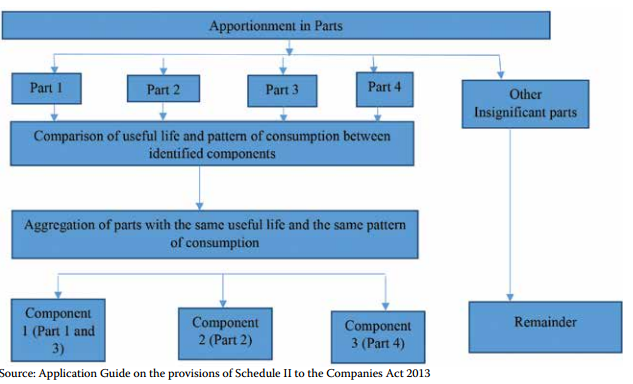

Let us first understand the concept of component accounting. There are two charges to profit and loss account representing costs relating to usage of a fixed asset. One of them is depreciation and the other is repairs and maintenance charge. Depreciation allocates the depreciable amount of a fixed asset over its useful life. There can be certain assets which comprise components whose individual useful lives differ significantly and thus require replacement from time to time within the estimated useful life of the principal asset. Aircraft is a classic example of such an asset. The airframe (i.e. the body of the aircraft), the engines and the interiors have different individual useful lives. The concern then is: what is the useful life of the aircraft? If the life of the airframe (being the longest of the individual lives of the three major types of components) is taken as the life of the aircraft, then how should the expenditure on replacement of interiors and engines during the useful life of the aircraft be dealt with? In certain cases, the components (usually small and low value) may require replacement very frequently, while in some other cases, the components may require replacement only once or twice during the estimated useful life of the asset (usually of high value) In order to overcome this concern, it is imperative that the components of a single asset are treated as different assets for accounting purposes. To illustrate this, suppose a composite asset costs R100. It has a major component X, whose cost is R40. This component is expected to have a life of 4 years while the rest of the asset is expected to have a life of 20 years. In the absence of component accounting, the position would be as follows: Thereby, it is evident that charging replacement cost of X in year of replacement would distort the true and fair view. However, if the aforesaid component is treated as a separate asset, the annual depreciation charge would be as follows: While the above is the best way of accounting for assets having major components whose useful lives differ significantly, practically there may arise a difficulty if a composite price has been paid for the total asset and also where there are a large number of individual components having varying lives which are shorter than the principal asset’s life. In such a case, apportioning the cost to components may present difficulties since the prices of all parts may not be available, or the aggregate price of all individual components may not necessarily be equal to the price of the composite asset. Moreover, such an exercise may be far too detailed and end up cluttering the fixed assets schedule. Hence, component approach is followed for parts of an asset which have significant costs and different useful life from remaining parts of the asset. Schedule II requires separate depreciation only for components of an asset having: (i) Significant cost, and (ii) Different useful lives from remaining parts of the asset. Determination of significant components requires a careful assessment of the facts and circumstances. This assessment would include at a minimum:

Comparison of the cost allocated to the item to the total cost of the aggregated property, plant and equipment; andConsideration of potential impact of componentisation on the depreciation expense.

For instance, a building may be split into components such as structural design, heating systems etc. Determination of components is a very judgemental exercise and due consideration should be given to all facts before concluding on component accounting A company needs to identify only material/ significant components separately for depreciation. For example, A Limited buys a machine for R500,000. The machine consists of four components, of which the cost of two components (with different useful lives) is R490,000. The remaining two components have a cost of R5,000 each, which is considered insignificant, and they have useful lives of four and six years respectively In the above example, we believe that the two insignificant components could be combined to give a cost of R10,000 and a useful life of five years. Accordingly, the machine would be split into 3 different components. Based on the above therefore, identification of separate components of an asset and determination of their useful life is not merely an accounting exercise; rather, it involves technical expertise. Hence, it may be necessary to involve technical experts to determine the parts of an asset.

Accounting for Replacement Costs

The application of component accounting will cause significant change in measurement of depreciation and accounting for replacement costs. Currently, companies need to expense replacement costs in the year of incurrence. Under component accounting, companies will capitalise these costs as a separate component of the asset, with consequent expensing of the net carrying value of the replaced component. The capitalised replacement cost will be depreciated over its estimated useful life (generally, till the time of next replacement), which should be lower than the life of the principal asset. If it is not practicable for a company to determine carrying amount of the replaced component, it may use the cost of the replacement as an indication of what the cost of the replaced part was at the time it was acquired or constructed. However, it is important to note that the dayto-day service cost for an item of fixed asset will be expensed and will not qualify for capitalisation.

Accounting for Major Inspection or Overhaul

Though Accounting Standard 10 Accounting for Fixed Assets does not comprehensively deal with component accounting, Ind AS 16 Property, Plant and Equipment provides guidance on this matter. Under component accounting as envisaged in IndAS 16, major inspection/overhaul cost is treated as a separate part of the asset, regardless of whether any physical part of the asset is replaced or not. Hence, companies, while preparing financial statements under Indian GAAP should draw an analogy from Ind AS 16. When the company purchases a new asset, it is received after major inspection or overhauling by the manufacturer. Hence, major inspection or overhaul can be identified separately at the time of purchase of new asset. The cost of such major inspection or overhaul is depreciated separately over the period till next major inspection or overhaul. Upon next major inspection or overhaul, the cost of new major inspection or overhaul is added to the gross block of the asset and any residual amount pertaining to the previous inspection or overhaul is derecognized. For example, C Limited runs a merchant shipping business and has just acquired a new ship for R10,000. The useful life of the ship is 15 years, but it will be dry-docked every three years and a major overhaul will be carried out. At the date of acquisition, the dry-docking costs for similar ships that are three years old are approximately R2,000. Therefore, the cost of the dry-docking component for accounting purposes is R2,000 and this amount would be depreciated over the three years to the next dry-docking. The remaining carrying amount, which may need to be split into further components, is R8,000. Any additional components will be depreciated over their own estimated useful lives. If the element relating to the inspection/overhaul had previously been identified, it would have been depreciated between the time of identification and the next overhaul. However, if it had not previously been identified, the recognition and de-recognition principles still apply. In such a case, the company uses estimated cost of a future similar inspection or overhaul to be used as an indication of the cost of the existing inspection or overhaul component to be derecognised after considering the depreciation impact.

Computation of Depreciation

Each significant component of the asset having useful life, which is different from the useful life of the principal asset, is depreciated separately. If useful life of the component is lower than the useful life of the principal asset as prescribed in Schedule II, such lower useful life should be used. On the other hand, if the useful life of the component is higher than the useful life of the principal asset as prescribed in Schedule II, the company can use higher useful life only if the component is expected to be used even after expiry of useful life for the principal asset. Presentation/Disclosure Although individual components are accounted for separately, the financial statements continue to disclose a single asset. For example, an airline would generally disclose aircraft as a class of assets, rather than disclosing separate information in respect of the aircraft airframe, engines, interiors, etc. Moreover, Schedule II requires disclosure of justification if a company uses higher or lower life than what is prescribed in Schedule II.

Transitional Provision

Accounting Standard 10, gives an option to follow the component accounting, however, it does not mandate the same. In contrast, component accounting is mandatory under the Schedule II w.e.f. 1st April 2015. Considering this, in our view, the transitional provision of Schedule II can be used to adjust the impact of component accounting. If a component has zero remaining useful life on 1st April 2015, its carrying amount, after retaining any residual value, may be charged to the opening balance of retained earnings. The carrying amount of other components, i.e., components whose remaining useful life is not nil as on 1st April 2015, is to be depreciated over their remaining useful life. Identification of Cost of Component as on 1 April 2015 Application Guide on the provisions of Schedule II of the Companies Act, 2013 states that, if the separate cost of each significant component of an asset is not available in the books of account, following criteria can be used:

(a) Break up cost provided by the vendor;(b) Cost break up given by internal/ external technical experts;(c) Current replacement cost of component of the related asset and applying value the same basis on the historical cost of asset

While the Application Guide does not clarify whether or not there is a free choice in applying the above criteria, it appears logical to apply the criteria in the chronological order in which they are stated above. Let’s discuss this concept by way of an example: Company A acquired a machine on 1st April 2011 for INR 100,000. The useful life of the machine was 20 years. As on 31st March 2015, the accumulated depreciation is INR 20,000 (machine costing INR 100,000 depreciated for four years with nil residual value), and corresponding WDV is INR 80,000 (INR 100,000-INR 20,000). Pursuant to Schedule II of the Companies Act, 2013, the company started following component accounting w.e.f 1st April 2015, wherein two components (A and B) were identified having an original cost of INR 20,000 and INR 80,000 respectively. The useful life of component A is estimated as 8 years (from the date of purchase) whereas the useful life for component B remains unchanged. Thus, the remaining useful life of component A as at 1st April 2015 is 4 years For allocating the carrying value to components A and B, one view is that the carrying value should be allocated as per the original cost of the components. As per this, the carrying value of component A i.e. INR 16,000 (i.e. original cost of 20,000 less accumulated depreciation of 4,000) will be depreciated over 4 years and that of component B i.e. INR 64,000 (i.e. original cost of 80,000 less accumulated depreciation of 16,000) will be depreciated over 16 years. An alternative view could be to allocate the carrying value to the components ‘on the basis of’ their current replacement cost. As per this, WDV of INR 80,000 will be allocated to components A and B in the ratio of their current replacement cost. Let’s assume that current replacement cost of components A and B is INR 10,000 and INR 60,000, respectively. Therefore WDV of INR 80,000 will be apportioned into component A and component B as INR 11,429 and INR 68,571 respectively. As stated above, while the Application Guide on the provisions of Schedule II of the Companies Act, 2013 does not clarify which is the preferred criteria to identify the cost of each significant component, it would be appropriate to use the original cost of acquisition as the basis, if the same is available.