The normal understanding of turnover or understanding under VAT/ CST would not be correct. The definition of “Aggregate Turnover” under GST needs to be understood.

New functionality on Annual Aggregate Turnover on GST Portal

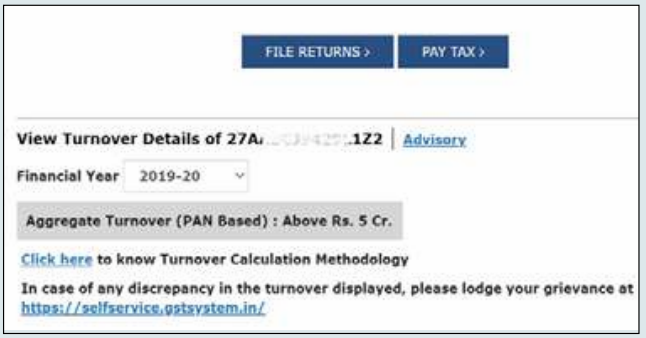

I am very happy to share the GSTIN most awaited functionality on taxpayers’ GSTN dashboards

The taxpayers can now see the Annual Aggregate Turnover (AATO) for the previous FY, instead of just the two slabs of Above or Upto Rs. 5 Cr.The taxpayers can also see the Aggregate Turnover of the current FY based on the returns filed till date

The TO calculation is based on the returns filed in the last financial year. For details of the calculation see the below Turnover calculation logic.

- For Normal Taxpayers who have filed all GSTR-3Bs: Turnover reported in GSTR-3B Column 2 of Table 3.1 {(a),(b),(c) & (e)} during the Financial Year 2019-20 have been taken into consideration (in case all the returns have been filed for the same).

- For Normal Taxpayers who have not filed all GSTR-3Bs: The following formula is used for extrapolation of turnover: (Sum of taxable value) X (*No.of GSTR-3B liable to be filed)/ (No. of GSTR-3B filed) *Categorisation of taxpayers to derive the number of GSTR3B liable to be filed I. GSTINs who are active as on date and were NOT IN composition during FY 2019-20, number of GSTR-3B liable to be filed have been arrived at as follows:

a. If the taxpayer is migrated, then No.of GSTR-3B liable to be filed is 12b.If the taxpayer is new and registered on or before 31st March, 2020, the No.of GSTR-3Bs liable to be filed shall be derived on the basis of GSTIN approval/grant date i.e. if approval/grant date is on or before April, 2019, then 12, else based on month of approval/grant of GSTIN (e.g. If the month of grant of GSTIN is May 2019, then number of GSTR3B liable to be filed is 11,if it is June 2019, then it is 10 and so on).

II. GSTINs who are cancelled as on date and were NOT IN composition during 2019-20, number of GSTR-3B liable to be filed have been arrived at as follows:

a. GSTINs registered on or before 31st March 2020.b. Months between cancellation date and approval/ grant date of GSTIN decides the number of GSTR3B liable to be filed.c. If cancellation date is beyond March 2020, then month between March 2020 and approval/grant Month of GSTIN is derived.d. If approval/Grant of GSTIN month is before April 2019, then month between cancellation date and April 2019 is derived.

III. GSTINs who are active as on date and were in composition BUT WITHDRAWN during 2019-20, number of GSTR-3B liable to be filed have been arrived at as follows:

a. GSTINs registered on or before 31st March 2020.b. Months between Withdrawal date and 31st March 2020 is defined as number of GSTR-3B liable to file.

IV. GSTINs who are cancelled as on date and were in composition BUT WITHDRAWN during 2019-20, number of GSTR-3B liable to be filed have been arrived at as follows:

a. GSTINs registered on or before 31st March 2020.b. Months between Withdrawal date and 31st March 2020 and cancellation date decides the number of GSTR-3B liable to be filed. c. If cancellation date is beyond March 2020, then month between March 2020 and Withdrawal Month of GSTIN is derived.

For Composition Taxpayers opted-in throughout the FY: Since the Annual Aggregate Turnover limit for opting in as Composition Taxpayer is up to Rs. 1.5 crore, hence the taxpayers under this category have readily been bracketed under ‘up to Rs. 5 Cr.’ of Annual Aggregate Turnover. Note: kindly check the below ‘Advisory’ on the aforementioned functionality

This facility shows to the taxpayer AATO (Annual Aggregate Turnover) based on the returns filed by him/ her in the last financial year.The facility of turnover update has also been provided to the taxpayer in this functionality, if the said taxpayer feels that the system calculated turnover varies from the turnover as per his/her records.As stated, the calculation is based on the returns filed in the last financial year. For details of the calculation see Turnover calculation logic.This facility of turnover update shall be provided to all the GSTINs registered on a common PAN. All the changes by any of the GSTINs in his turnover shall be summed up for computation of Annual Aggregate Turnover for each of the GSTINs.The taxpayer can amend the turnover twice within a period of one month from the date of roll out of this functionality.Thereafter, the updated value shall be frozen with no further attempts provided to the taxpayers to amend their turnover(s) and this turnover figure will be sent to the Jurisdictional Tax Officer for review.In case the jurisdictional Officer finds any discrepancy in the updated/amended values furnished by the taxpayer, the said officer can amend the turnover.Tax officers are expected to consult and/or communicate with the taxpayer before amending the turnover declared by the taxpayer.The turnover finalized by the tax officer after such consultation shall be considered final.In case no action is taken by the officer within 30 days on the turnover reported by the taxpayer, the same shall then be considered final (which will be displayed to the taxpayer accordingly) and will be considered as such for the entire previous financial year.In case of any grievances pertaining to the said functionality, the aggrieved taxpayer can raise a ticket at https://selfservice.gstsystem.in.All such tickets shall be investigated by the technical team and shall be resolved on a case by case basis and when needed they shall be forwarded to the jurisdictional officer.

Aggregate Turnover under GST Regime

- Turnover, in common parlance, is the total volume of a business. The term ‘aggregate turnover’ has been defined in GST law as under: “Aggregate turnover” means the aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis), exempt supplies, exports of goods or services or both and inter-State supplies of persons having the same Permanent Account Number, to be computed on all India basis but excludes central tax, State tax, Union territory tax, integrated tax and cess.

- The aggregate turnover is a crucial parameter for deciding the eligibility of a supplier to avail the benefit of exemption threshold of Rs. 40 Lakhs [Rs. 20 Lakhs in case of special category States except J & K] (new limit from 1st April 2019 ) and for determining the threshold limit for composition levy. Let us dissect the definition in small parts to understand the meaning clearly. There are certain terms used in the definition which need a bit of elaboration.

- It may be noted that the inward supplies on which the recipient is required to pay tax under Reverse Charge Mechanism (RCM) does not form part of the ‘aggregate turnover’. The law stipulates certain supplies like, Goods Transport Agency services, services received from outside India, to name a few, where the recipient of service is made to pay the tax. The value of such supplies on which tax is paid, would not form part of the ‘aggregate turnover’ of recipient of such supplies. However, the value of such supplies would continue to be part of the ‘aggregate turnover’ of the supplier of such supplies.

- The second element of value which would not be included in the ‘aggregate turnover’ is the element of central tax, state tax, union territory tax and integrated tax and compensation cess.

- The value of exported goods/services, exempted goods/ services, inter-state supplies between distinct persons having same PAN would be added to ‘aggregate turnover’.

- Last but not the least, such turnover is to be calculated by taking together the value in respect of the activities carried out on all-India basis.

- The aggregate turnover is different from turnover in a State. The former is used for determining the threshold limit for registration as well as eligibility for Composition Scheme. However, the composition levy would be calculated on the basis of turnover in the State.

Analysis of ATO

The definition of ATO. Sec. 2 (6) – means the aggregate value of all taxable supplies( excluding the value f inward supplies on which tax is payable by a person on a reverse charge basis), exempt supplies, exports of goods or services or both and interstate supplies of person having the same permanent account number, to be compluted on all India basis but excludes central tax, Union territory tax, integrated tax and cess. The definition of exempt supply. Sec 2(47) – means supply of any goods or services or both which attract nil rate of tax or which may be wholly exemption from tax under section 11 or under section 6 of the Integrated Goods and service tax Act, and includes non taxable supply.

ATO would there fore include the following:

i. All taxable supplies other than reverse charge.ii. All supplies with distinct entities including interstate- Same PAN different GST registrations (in different States or separate business vertical).iii. Supplies of agents/ job worker on behalf of the principal.iv. Goods supplied / received back to/ from job worker on principal to principal basis.v. Exempt supply: exempt under notification, non taxable supplies ( Specified Petroleum Products like Diesel, Petrol, Liquor etc.vi. Export or zero rated supplies.vii. Taxes other than those under GST

ATO would exclude the following:

i. Inward supplies (including those under reverse charge)ii. Taxes and cesses under GSTiii. Goods sent for or received back under job work u/s 143iv. Intra state suppliesv. Interstate supply of servicesvi. Transactions which are neither supply of services or goods: employee to employer, services by court or tribunal, MP, MLAs, posts as per Constitution of India, land or completed building and actionable claims other than betting, gambling or lottery.vii. Supplies provided and received outside India (Global business)

Recommended –